As Featured In:

In our previous blog post, Use the Bucket Plan to Secure Your Dream Retirement, we mentionedone of the biggest mistakeswe see retirees make. In this article, we would like to dive deeper into what that mistake is, why it can be so damaging to a retiree’s future wealth, and how we help clients manage and minimize this risk.

Imagine you're planning a road trip and need to fill up your gas tank along the way. Let's say you encounter some unexpected detours, like steep hills or winding roads. If you hit these obstacles when gas prices are high, you end up spending a lot more money on fuel, leaving you with less cash for the rest of your journey.

Similar to the price of gas, we cannot predict future market returns; therefore,one of the biggest mistakesretirees make is failing to plan for the combination of market volatility and withdrawing money from their investment accounts, also known as Sequence of Return Risk. In retirement planning, sequence of return risk is like those unexpected detours. It's the risk that the timing of when you retire or start withdrawing money from your investments coincides with a period of poor market performance. Just like those pricey gas stops, experiencing market downturns early in retirement can significantly reduce the overall amount of money you have available throughout your retirement years. This can make it harder to sustain your desired lifestyle and potentially even derail your retirement plans.

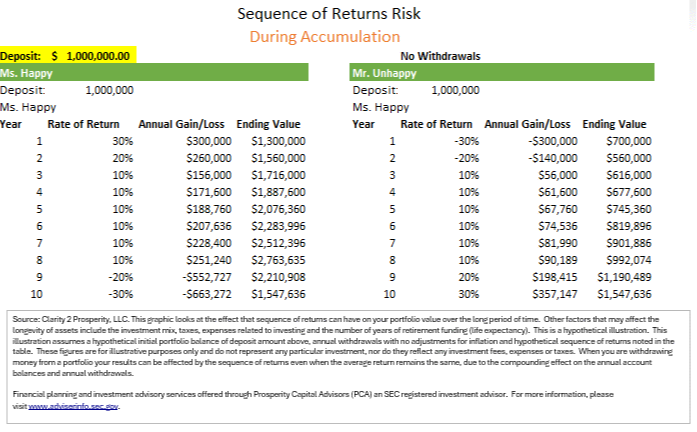

When you are in your accumulation years, the timing of your investment returns do not matter asmuch as they do when you are in your distribution years. Let’s look at two portfolios over a 10-year period. They begin with the same starting balance. There are NO withdrawals during the 10 years. The only difference is the order of returns, meaning they both average a 6% average annual return. However, the order of the returns each year is different. The first portfolio experiences strong returns in years one and two and negative returns in the last two years; the second portfolio experiences the opposite: negative returns in years one and two and two strong return years in years nine and ten. At the end of the 10-year period, both portfolios have the same ending balance! When you are not withdrawing money, the order (or sequence) of your returns do not matter.

Now, let’s enter the distribution years of retirement.

A portfolio invested in stocks and bonds is subject to volatility. For example, a 60/40 stock-to-bond portfolio may experience a -30 % or +30% return or anything in-between in any given year! And market prognosticators rarely get their predictions right. This means that the market returns you may experience after you retire are down to the luck of the draw! And this paradigm continues throughout your retirement; meaning having a plan to continuously manage sequence of return risk throughout your distribution years is important.

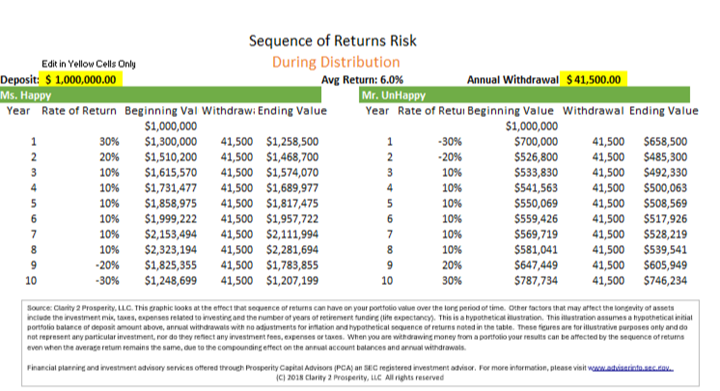

To illustrate, let us tell you the tale of Alice and Bob. Alice (we’ll call her Ms. Happy) experiences good market returns right after retiring, while Bob faces several bad returns in the first couple of years.

Alice's retirement journey begins with a stroke of luck. She enjoys strong investment growth, allowing her savings to continue growing even as she starts withdrawing money for living expenses. Although her investments at retirement started with $1 Million dollars, and over the next 10 years she withdrew a total $415,000, ($41,500 per year), at the end of year 10 she had a portfolio balance of $1,207,199. With this positive start, Alice can comfortably stick to her retirement budget, take vacations, and pursue hobbies without worrying too much about her finances.

On the other hand, Bob's (Mr. Unhappy) retirement starts off on a rocky road. The market experiences a downturn for the first two years after he retires, causing the value of his investments to plummet. Bob still needs to withdraw money from his retirement accounts to cover his living expenses, but now he's selling investments at a loss. As a result, Bob's retirement savings take a hit, and he watches helplessly as his nest egg dwindles faster than expected. Remember, Bob started with the same $1 Million dollars and withdrew over the first ten years of his retirement the same $415,000 as happy Alice. The average return over those 10 years was the same, the only differencewas the ORDER of those returns. Bob’s ending value is $746,234 (which is $460,965 less than Alice!)

Despite having the same amount saved for retirement as Alice, Bob finds himself in a tough spot. He may need to cut back on his spending, delay major purchases, or even consider going back to work to make ends meet. Meanwhile, Alice continues to enjoy her retirement without financial stress, thanks to her fortunate timing with the market.

This illustrates the impact of sequence of return risk. Even with the same amount of savings, the timing of market returns can significantly affect retirees' financial well-being in the early years of retirement. It emphasizes the importance of careful planning and diversification to mitigate the risks associated with market volatility during retirement.

If you can’t predict market behavior and you understand that your money will need to grow over a several-decade retirement to combat inflation, what can you do?

Imagine if Bob had divided his retirement savings into different "buckets" based on the time horizon for when he planned to use the money. One bucket could contain enough cash or highly liquid, conservative investments to cover his living expenses for the first 5 years of retirement, while the remaining buckets could be allocated to longer-term investments with higher growth potential. With this approach, even if Bob faced poor market returns in his early retirement years, he wouldn't need to sell his long-term investments at a loss to cover his immediate expenses. Instead, he could rely on the cash and conservative investments in his Income bucket, allowing his other investments more time to potentially recover from market downturns.—and refill his Income or “Soon” Bucket when necessary, likely leading to a higher ending value at year 10.

Knowing that he has a cushion to withstand short-term market fluctuations, Bob would likely feel less stressed about his finances. This emotional resilience can be invaluable during challenging market conditions, helping him stick to his long-term financial plan without making rash decisions.

One of the biggest mistakes we see pre-retirees making is going straight from their “accumulation” years into their distribution years without planning for the indiscriminate roller coaster ride that is the financial markets. When we work with our distribution clients, we explain that preserving some of their capital into time-segmented buckets is an example of how planning manages risk and helps them avoid being negatively impacted by market volatility. In fact it helps them use volatility to their advantage! Done correctly, it should help them enjoy the ride!

If you want to approximate what the impact of experiencing market downturns early in retirement may mean to you, you can download our simple Sequence of Return Calculatorhere.